LPG price parity

The GMA used Leach & Oduro (2015) and Scott et al.’s (2017) processes for comparing energy delivered to the pot to show which fuels are most cost-effective in each country. Price parity is represented by a solid line. For countries appearing above the line, it is cheaper for their citizens to cook using the fuel on the horizontal axis and for those below, the fuel on the vertical axis. Significant opportunities exist when large proportions of the population are cooking with the fuel on the nearest axis, as they would save money by switching to the fuel on the opposite side of the parity line.

However, we are going to have to revisit these in the light of the gains from Electric Pressure cookers. The following price parity analyses present conservative estimates for the opportunity for eCook, with regards to both the cost of electricity and the efficiency of an electric stove. Also many countries have a lifeline tariff, ranging from free for an initial number of kWhs per month, to a gradually increasing rate depending on use (rising block tariff). The graphs are based on the full price domestic tariff in each country and do not take into account lifeline tariffs. In addition, the price parity plots are based upon using a simple electric hotplate with 70% efficiency. However, a huge range of energy-efficient electrical cooking appliances are already available on the market (e.g. microwave, electric pressure cooker, induction stove), which could well open up new markets in contexts where these are compatible with local cooking practices.

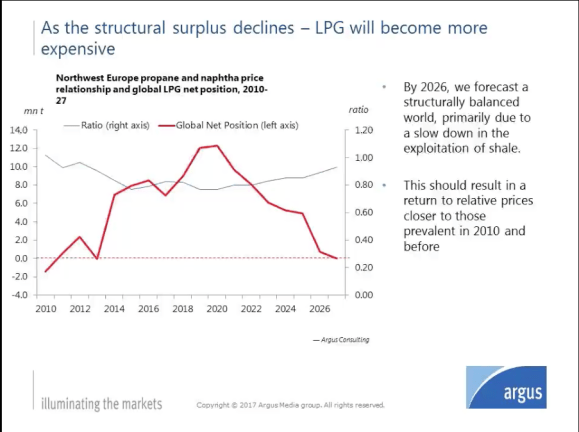

LPG is significantly cleaner than ‘polluting fuels’ and has an important role to play as a transition fuel, however it does not offer a truly sustainable long-term pathway to clean cooking. It can easily be compressed, facilitating distribution, allowing it reach far beyond the limits of the piped networks in which natural gas is distributed. However, as a fossil fuel, it is a finite resource and still contributes to climate change. What is more, whilst falling LPG prices are opening up new markets around the world, Argus Consulting (2017) note that these markets are developing in a bubble. The development of fracking enabled the exploitation of shale gas that was previously uneconomically recoverable. The world is currently “LPG long”, as it is co-produced alongside other petroleum products that are in higher demand. Consequently, Figure 20 shows Argus Consulting’s (2017) predictions of continually falling prices until 2020, followed by a return to 2010 levels by 2026.

Argus Consulting’s (2017) global LPG supply/demand modelling results.

The availability of cheap LPG presents strong competition for grid connected HHs, as the majority of countries fall under the LPG/electricity parity line. Island nations generally have high fuel prices as long supply chains for imported fuels significantly increase prices. However, grid electricity is often also expensive, as many small island nations rely on diesel mini-grids, which also run on imported fuel. In a number of African countries with limited LPG markets, such as Uganda, Gambia and South Sudan, reportedly high LPG prices seem to make switching to electricity cost effective. However, as the LPG markets in these countries develop, the cost is expected to fall.

Nevertheless, an opportunity still exists in some African countries with established LPG markets and low retail prices, such as Ethiopia and Sudan, where the price of grid electricity is so low that it is still cost effective to cook with it. In fact, as a general trend, although figures suggests that global LPG prices can be expected to fall until 2020, further opportunities are likely to emerge after this date as global LPG demand begins to catch up with supply. As would be expected, the figure below shows a correlation between LPG price and the number of users, likely due to the iterative process of economies of scale bringing down the price and a lower price encouraging greater adoption.

LPG market attractiveness.

Countries coloured by region: AIMS, Central Africa, Central America & Caribbean, Central Asia & North Korea, East Africa, Europe, India & China, Middle East , North Africa, Pacific Islands & PNG, South America & Mexico, South Asia (excl. India), Southeast Asia, Southern Africa and West Africa. Two-letter country codes listed in the GMA report Regional colour coding and two-letter country codes.